Individuals who purchase and pay for Tax-Qualified Long-Term Care Insurance policies for themselves, their spouses, and their tax dependents may claim the premiums paid as deductible personal medical expenses if the Individual itemizes his or her taxes (See Internal Revenue Code (IRC) Sec. 213(a) and IRC Sec. 213(d)(1)(D)).

However, any Tax-Qualified Long-Term Care Insurance expenses are deductible only to the extent that the individual’s total unreimbursed medical care expenses exceed 7.5% of his or her Adjusted Gross Income.

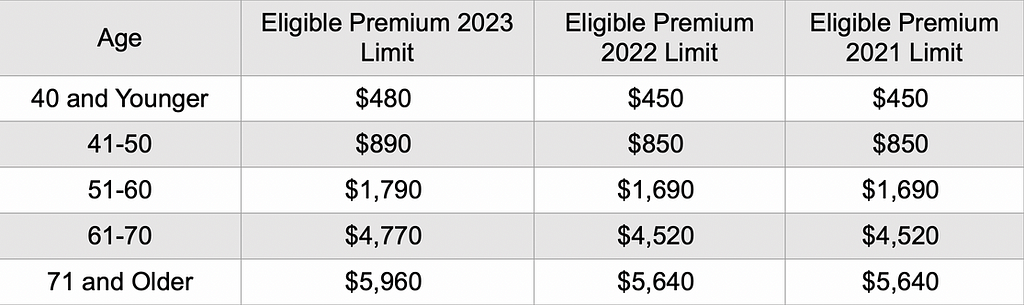

Further, the amount of the Tax-Qualified Long-Term Care Insurance premiums that may be deducted is subject to the following dollar limits based on the insured’s attained age before the close of the tax year (IRC Sec 213(d)(10)).

We do not provide tax or legal advice. Any decisions whether to implement these ideas should be made by the client in consultation with professional financial, tax, and legal counsel.